In the global macro picture, as some questions become answered, more uncertainty arises. This week was highlighted by the conclusion of the presidential election, and subsequently markets tanked. This is not to say that the election of a democratic incumbent is the catalyst. Rather, ourfocus is shifted to more pressing matters. Earnings season is still in session, and continues to follow its general trend. Companies have navigated their way to earnings outperformance, but revenues remain light. As long as the global environment remains clouded with doubt and negative sentiment, the integrated global companies of modern times will continue to come up short on revenue. McDonald's (MCD) is a perfect example of a global company that is struggling to handle the fragile economic environment. The company reported disappointing numbers this week that pinned its failure on the global nature of its business.

(Click on graphics below to enlarge)

Similarly, fear out of the U.S., Europe, and China littered headlines after the election. There has been constant news coverage of the impending "fiscal cliff" and the deepening of European troubles. Upon the election's completion, both parties came out to discuss their stance on the U.S.debt situation. The tones remained subdued, but the content was little changed. Both sides remain stark on their viewpoints and memories of the debt ceiling of a not so distant past come to the forefront. Although theU.S. has its troubles, the EU is in the same boat, if not deeper underwater in the court of public opinion. The ECB had a meeting this week where the outlook remained negative and the contagion to core countries was presented as a pressing matter. Greece quarreled endlessly about its depletion-of-funds dilemma and its effect on the general public. France's health has been called into question, and Germany is looking to provide answers to avoid further crisis. As well, Spain is still playing the game of chicken with bond markets over when it will seek further aid from the ECB.

The question turns to how the market perceives this constant influx of news. The health of both the dollar (UUP) and euro (FXE) looks suspect, but the pair shows that the favor leans towards the dollar for now. A breakout lower from a fairly symmetrical triangle highlights the euro regions weakness. They have multiple countries with deepening issues, and seemingly few avenues to turn to that stimulates growth. A weakereuro is better for the region, and looks to continue its downtrends as activity slows and recessions grow worse.

The dollar is not in a favorable position overall though. Looking at the spike in the yen (FXY) /dollar pair highlights its resounding weakness. As long as the U.S. struggles with internal issues, investors will look elsewhere to store their capital.

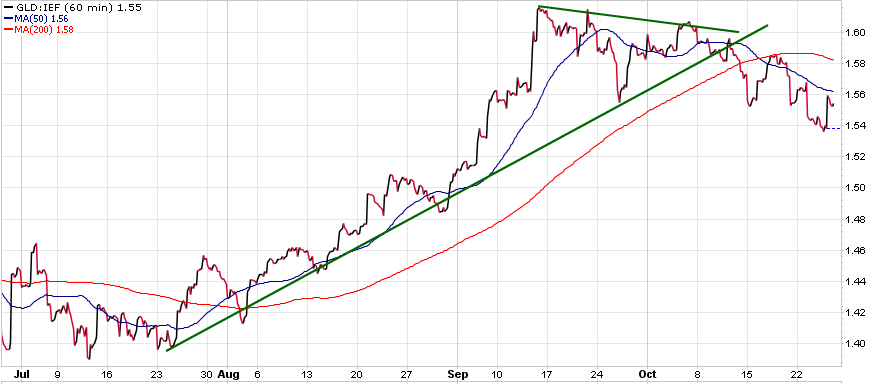

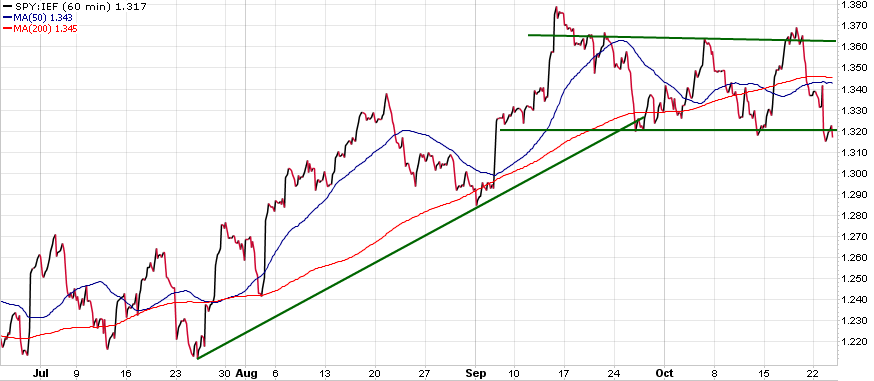

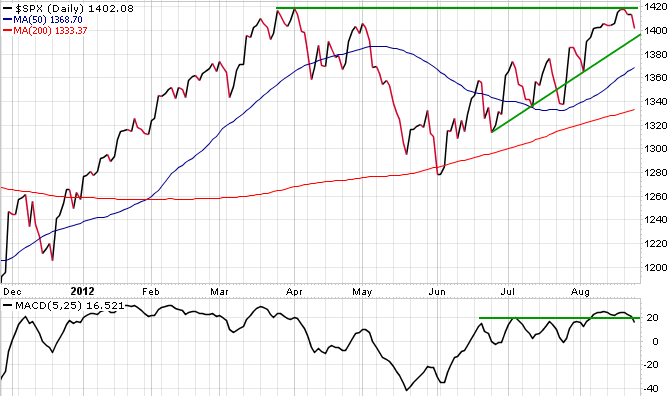

Equity markets witnessed a downturn in the risk off environment following the election as well. The culmination of less than impressive earnings and fear of global recession worried markets. An indicator highlighting the current sentiment is that of investment grade corporate debt (CORP) over equity markets (SPY).

Junk has seen its run, but corporate debt is well-positioned currently. Sovereign markets are riddled with debt, and a suitable alternative looks to be healthy U.S. corporations. Low debt loads, adequate cash coverage, and the ability to navigate tough economic environments are causing more eyes to turn to such assets. The pair below has a strong negative correlation to risk assets and has conveyed the underlying pessimism surrounding markets recently. This past week the indicator saw a breakout higher, which alongside an equity break below its 200 day MA, bodes negatively overall for risk. Look for further pessimism in future sessions as long as investors are favoring corporates to equity.

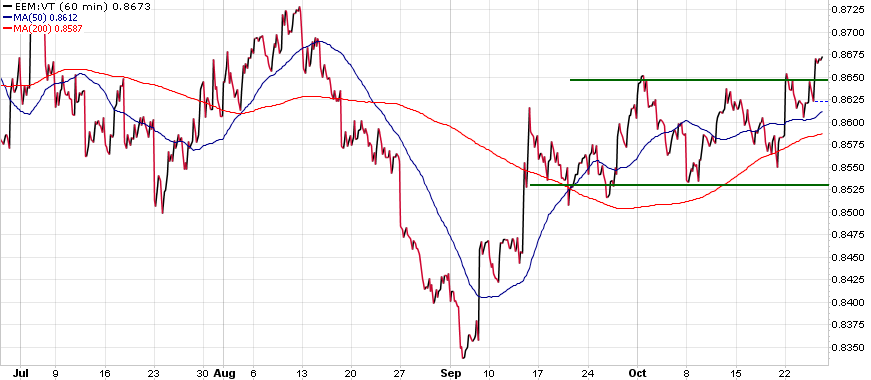

The last indicator of interest in the global picture is the apparent loss of steam in Chinese equity (FXI). China showed extreme weakness earlier in the year, prompting many to call for some form of aid from the government. As central banks began to stimulate and sentiment rose, China regained its footing and outperformed world equity (VT) as seen below. The problem now is that re-occurring stressors from Europe and the U.S. threaten China and its export market. If the world falls, China is not immune to catching the cold. The chart looks to be in a period of consolidation and a rounding top. Further downturns in other strategically important regions across the world will weigh on this indicator.

Much has been revealed over the preceding days, which has pushed caution into the picture. The problem with climbing a wall of worry is that as more mounts on top of you, you are destined to cave eventually.