Since the inception of Quantitative Easing, many have debated its diminishing returns quality. Although easing does manipulate true market action, this is not to say it harms it. Speculation surrounds what will happen when it is all said and done, but currently, QE has brought into existence a Bernanke Put of sorts. The Fed was initially created to aid in times of crisis, in order to limit its effects. With the macro picture as it stands, the Fed looks to provide liquidity and limit loss. Diminishing effects implies a lesser pop on announcement, but a pop is superior to a downturn. Markets turned higher today on dovish tones from the fed; which begs the question, do you prefer capital preservation to margin calls? Gradual growth has been expected, but high unemployment for too long leads to structural damage. This damage could lead to far reaching issues, and could even be magnified with a weaker global picture. The Fed realizes this, and says it stands ready.

As evidence to the fact that a Bernanke Put improves market confidence, consumer sentiment rose to its highest level since May. Although uncertainty has littered the air, the belief in a floor of future despair kept sentiment high. As long as hope remains in markets, sell offs should not be overly drastic. Bernanke controls what he can, but Draghi and Germany have issues in their own right. Further announcements should keep markets on their toes for the better part of September.

The first quantitative chart to be discussed is inflation protected treasuries (TIP) vs. 20+ year treasuries (TLT). This ratio gives room to the idea of more easing. As inflation and economic growth expectations diminish, the indicator falls. It correlates strongly with risk assets, but has shown price weakness lately. This indicator usually bottoms prior to QE announcements, but as of late, it has kept falling. It is not to say we are as bad off as in 2008, but the Fed was right in its remarks. Growth is between the realm of gradual and anemic, which will further dampen outlooks unless corrected.

Along the same lines, commodities prove to be an indicator of global market health. The ratio of commodities (DBC) over treasuries shows the markets are reverting towards lower trend lines. It broke out higher in mid June and has led throughout the current rally. However, the macro picture still has many questions to be answered, and until they are, commodities won't continue to lead. The MACD tracking this indicator has broken lower, but sees resistance at the zero level. The solutions to be unturned in the near future will determine its direction.

In order to see things that the market doesn't, it sometimes requires obscure methods. In this case the obscure indicator is Put/Call Equity indicator over gold (GLD). Put/Call moves inverse to equity markets and gold moves purely on supply/demand. As calls are accumulated, bullish sentiment rises. However, to put this single aspect to the test, one can add another leg. Gold acts as a weight of sorts, and when calls or puts are being accumulated with vigor, the indicator will show it. The weight adds to the already strong inverse correlation, and as can be seen, there is some upward break. This is bad for risk assets, including equities. It will need to continue lower for sentiment to remain intact.

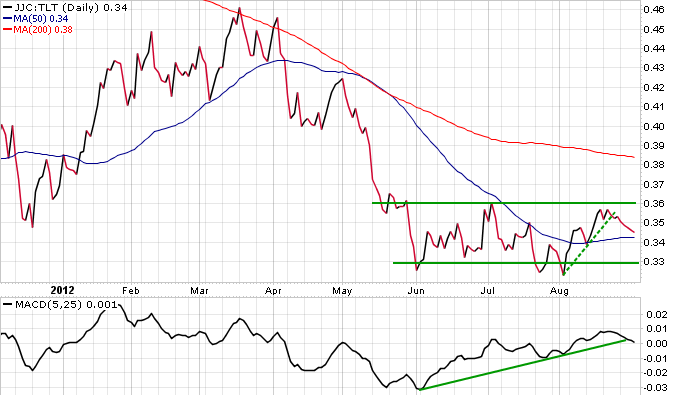

The last price ratio contains copper. Copper is said to be a solid indicator of economic outlook and this indicator confirms it. Copper (JJC) over treasuries correlates around .93 with equity. It has been range bound for much of the current risk rally, but looks to be showing weakness now. The break of both its price action and MACD underlying indicator are bearish for copper and risk as a whole. The fundamentals driving the move are weakness and lack of clarity out of China, as well as a struggling Aussie Dollar/Asian equity. The fed announcement should aid its move, but economic strength is the real catalyst.

Overall markets have a perceived put in place. This is due to the belief that Bernanke and Draghi stand ready for action. The only downside is if a macro situation unfolds that compromises their ability. If they begin to look overwhelmed at any point, then markets will break lower with force.