The macro trade currently requires a three pronged approach. The only way to navigate is to keep a keen eye on US, China, and European revelations. Markets spiked on the idea that the Fed could stimulate, but backed off when they questioned its probability. The biggest wrench in the easing debate currently, is whether economic data has improved enough to not warrant it. However, the minutes were clear, enough so to diminish much of the perceived vagueness. There was a call for substantial and sustainable economic data growth in order for the Fed to back off further easing measures. The data to date has been sporadic, and looking at indicators on a moving average basis, you will be hard pressed to find a clear upward trend.

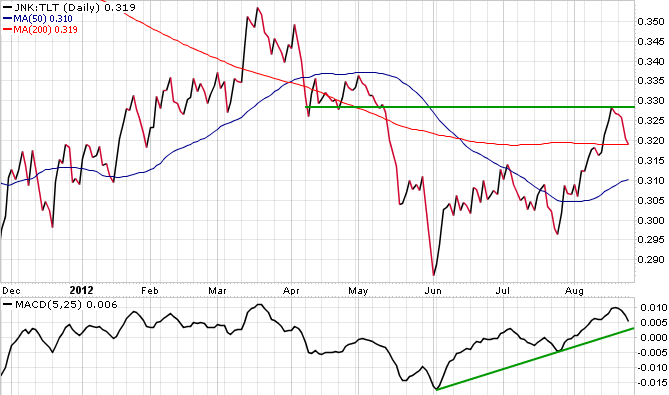

The first chart is that of junk debt (JNK) vs. 20+ year treasury (TLT), this indicator correlates well with the risk on markets. The ratio hit a wall of resistance, and with lack of substantial and positive evidence, it receded lower. Junk was yielding record low rates, and the run up even had Pimco cutting its exposure to the field. There is certainly room for a move higher, but this looks to correlate with further news to catalyze markets upward.

The next ratio of importance is European financials (EUFN) vs. the global equity market (VT). With so much hanging around the dealings of Europe, in both its Sovereign and Corporate debt markets, this indicator has a lot of sway. There looks to be improvement in the leadership, and meaningful plans seem to be in the works. The indicator must outperform in order for global confidence to regain its footing. The ability of both peripheries and core countries to decide on realistic plans, flexible and pragmatic, will lead to improved sentiment around the region. Sentiment has driven European yields, and cohesion amongst the group will only lead to more advance. The indicator looks to have reached resistance until further progress is made. Look for action in September to greatly influence its move higher, or lower.

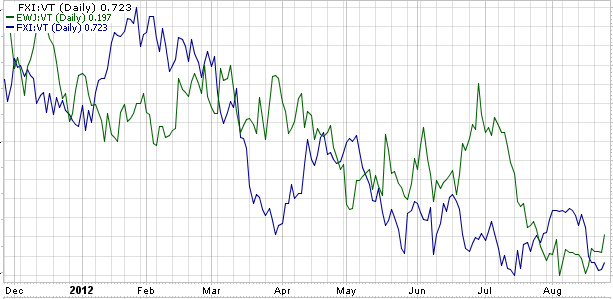

A move to the Far East presents a gloomier appeal. The indicators of choice are China (FXI) vs. world equity and Japan (EWJ) vs. world equity. Both markets have vastly underperformed over the past nine months. The shrinkage of exports in both is a concern, and can be attributed to a weaker global economy. Japan's drastic currency appreciation has done nothing to help its cause. Weak equity environments highlight each regions economic issues, and signal the need for relief. A move from the PBOC could moderate such declines, and would be positive for risk across the board.

An externality from a stronger Asia would be stronger commodities. The indicator in question is that of Copper (JJC) vs. 20+ year treasuries. This indicator shows strength in the face of inflation, and some form of easing out of China will prop it up. Risk on markets, as a whole, have moved on the notion that someone in the developed world would make a move to stabilize their economy, and copper has similarly oscillated alongside the idea. A move by at least one of the central banks should traject copper upwards, and out of its range.

Keeping this premise in mind, another market to watch is emerging equities. Emerging equity (EEM) vs. the world equity market, has a vested interest in China and the global economy as a whole. This indicator has been somewhat breaking down lately, and must show strength for confidence to return to the macro economy. The ratio's MACD indicator has been oscillating between bull and bear territory for months, and looks to make a move on more tangible evidence out of the developed world. Its hand being in commodities and exports as a whole, requires a stronger environment of operation. Until that environment is produced, this indicator will show weakness.

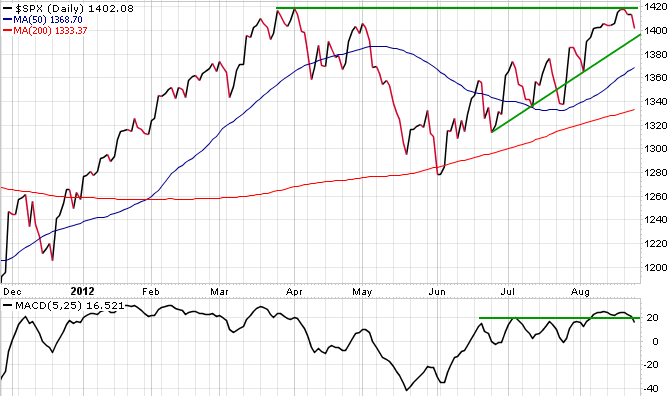

The last chart is that of the S&P 500 (SPY). Many people believe that the expectation of QE has led to the pricing in of its move in totality. Basically, that the market has run its course. The volumes have been low, but this was expected until tangible evidence was produced. Along the same thought, no meaningful breakout should be conceded until more evidence is shown. Based on the indicators above, equities do look to have more room, considering much of its suppression has been derived from the aforementioned problems. If problems are meaningfully fixed, why shouldn't risk breakout to new highs?