The current macro trade hinges on the move of central bank stimulation. Markets have become exuberant at the thought of accommodative monetary policy that should support risk assets. The current economic factors that have sustained this belief come in the area of weak inflation data, followed by weak inflation expectations. With Germany also showing weakness in recent economic releases, there could be more proof that a catalyst is in order.

click to enlarge images

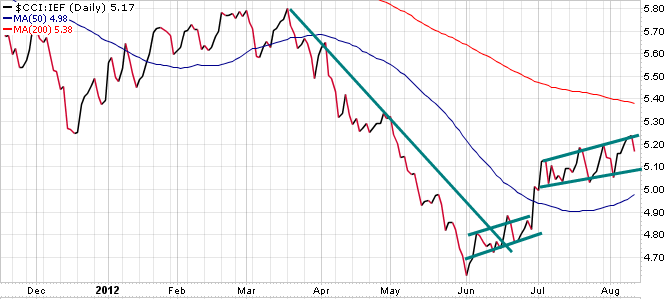

When monetary policy becomes accommodative, assets such as commodities should show signs of appreciation. The equal weight CRB index (CCI) tracks the very commodities that will benefit from the measures. The above chart shows commodities relative to risk off 10 years (IEF). The initial move higher followed the equities inverse head and shoulders breakout (SPY), and the current upward channel has been in line with the equities move as well.

Along the same logic, gold (GLD) now trades as a risk asset and should also move with equities. After the selloff equities have been able to push higher, yet gold has been in a gridlock with the 10 yr. note throughout the duration. However, the divergence between the price action and the MACD oscillator signals a different story. The oscillator has been trending higher for 3 months and now sits in a bullish range. A breakout higher from the price action should be followed by MACD strength and be further support for an equities rally.

Inflation Indexed bonds (TIP) tend to catch demand in inflationary environments, and have shown strength in the face of current monetary stimulus. The chart above again confirms the equities move higher, and give signs of a move higher in commodities (DBC) across the board. The cross tends to move inverse to the dollar (UUP), so look for dollar weakness in the near future.

A turn to more equity centric measures brings us to the cross of Consumer Staples (XLP) and the broader market (IVV). Consumer Staples littered the headlines during the downturn recently, praised as solid dividend plays and promises of stability in a shaky market. However, with broader strength, a sideways pattern has emerged in the cross. Similarly, the MACD oscillator has shown weakness since mid June. With a downside breakout the SPY should find strength in the current trend.

One of the final measures that will be looked at is the European financial sector (EUFN) compared to global equities (VT). The performance of this cross has spoken volumes in the risk vs. risk off trade recently. With the breakdown of financial institutions in Europe --- most notably in Greece, Ireland, and now Spain --- the political debate has surrounded around its resolve. In the current US rally, European financials have shown a period of consolidation. The path of least resistance has been up for now, yet a break in either direction for this cross will sway the direction of the broader markets over the intermediate term.

The culmination of this article resides in the trade of long Dollar and short Euro (FXE). The trade has been negatively correlated with equities and looks to be showing some weakness as of late. The break higher in May moved alongside a steep fall off for the SPY, but the overall trend looks to be rounding off at an intermediate top. The aggregation of price action and the preceding asset crosses above seem to point to near term weakness in the trade. The price is near a trend line and the MACD oscillator is in negative territory, which hints at a bearish undertone.

With the expectation of low inflation in China signaling further easing, and the BOE favoring easing to interest rate cuts, the environment looks to be shaping up for risk asset appreciation. Along the same, Germany is weakening which may open them up to more accommodative measures, and provide relief to a distressed region. Look to breakouts in the crosses above to signal the next step, but from what looks to be shaping, strength seems probable.