An interesting development crossing the headlines recently has been the lack of leadership in traditional bullish signals. The indicators in question are Russell 2000 (IWM) vs. Russell 1000 (IWB) and Transports (IYT) vs. Industrials (DIA). The divergence has just recently taken shape within the past year, and points to the fact that we are in a defensive rally. The lack of confidence seen in the markets seems to be a culmination of various factors. First is the volatility created by mishaps and market uncertainty. The presence of competing with and trying to outguess central bank actions has investors on edge, as well as market manipulating factors such as Knight Capital and other sentiment sapping developments. The next theme that has kept investors in defensive sectors is the search for yield. Many of the larger cap stocks offer less volatility, as well as yields unseen in the current low-risk bond markets. The defensive rally has many traders awaiting a cliff, and many others sitting on the sidelines letting gains pass them by.

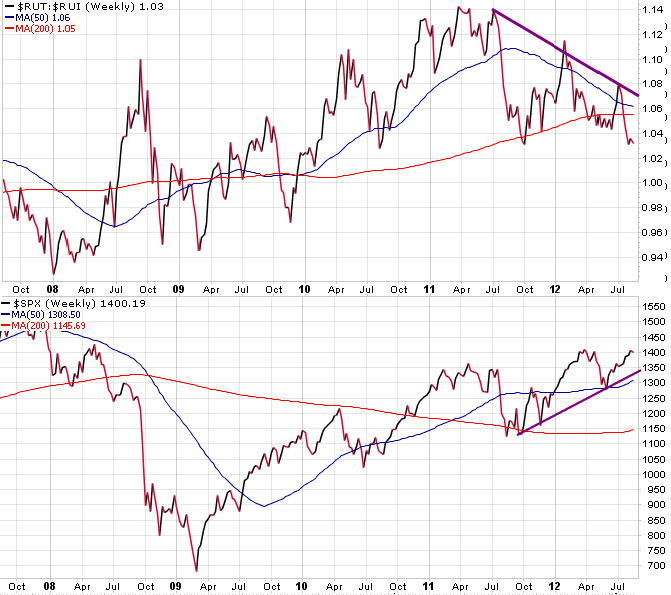

Above is a five-year chart showing the relative strength of transports and industrials. The divergence is evident, and again, has led to many questioning the move's strength. The idea is that companies that ship should be performing as well, if not better, than the companies that produce. Similarly, the small cap Russell 2000 should outperform the Russell 1000 as a sign of risk tolerance. By putting one's money into riskier small caps, investors are signaling their trust in the economic environment. The chart below shows that too is not the case.

The chart shows again a negative divergence over the past year. This may cause some alarm, as it has already, but in comparison to other indicators, the equities show room for strength. The charts of both Utilities (XLU) and Consumer Staples (XLP) vs. the broader market (SPY) are shown below. As a risk off trade, these pairs should fall in strong markets. They have been oscillating within a range over the extended period of uncertainty within the financial markets, but they look to be breaking out lower in the near future. This may be a signal that ignites money coming off the sidelines, and brings belief to the rally.

The final chart below is a somewhat alarming development within the move higher. It is true that energy stocks (XLE) should lead within a rally, but it is far and away leading this breakout. The rebound off of extremely weak levels and the diminished belief that the global economy would be thrown into a tailspin has aided XLE's move. Geopolitical risk is also somewhat weighted into the move higher. The only other times the pair had shown this much weakness was just before both QE1 and QE2 in 2008 and 2010 respectively. In all, it is not fair to say that an equity rise is leading to a gain in the XLE, so this somewhat compromises the strength. But with a shift from defensive into more cyclical sectors as a whole, sentiment should improve.